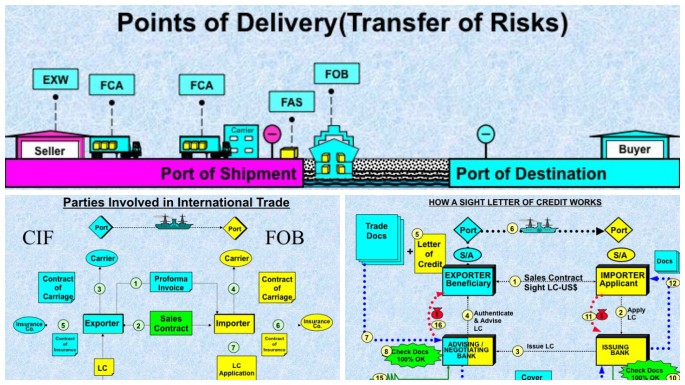

Under documentary collection method – there is sight and usance collection. For sight documentary collection it’s called DP (or Documents Against Payment), for usance it’s called DA (or Documents Against Acceptance).

1. In this presentation on Documentary Collection Method , we have the exporter (also known as Principal) and the importer (also known as Drawee). Both of them entered into a usance sales contract whereby the importer has agreed to give to the exporter 90 days credit terms which is expressed as 90 days after sight. They agreed that method of payment will be by usance Documentary Collection Method ie DA or Document against Acceptance.

2. Once the contract has been signed, the exporter will ship out the goods to the importer via the shipping agent.

3. After the exporter shipped out the goods, the exporter will prepare the necessary trade documents including the Bill of Lading and a Usance Bill of Exchange. .

The exporter will then prepare a cover letter which is also known as a Collection Instruction containing complete and precise instructions. The Collection Instructions form is normally prepared on a standard format given by the bank. The exporter will then forward all the trade documents as detailed in the Collection Instruction to his bank, the Remitting Bank in this case – ABC Bank.

Basically, the Exporter is informing the Remitting Bank that he had shipped all the goods to the Importer. And the Exporter has wants the Remitting bank to send all the trade documents over to the importer and to collect payment 90 days after sight on his behalf. What does 90 days after sight means? Importer must pay the Exporter 90 days after acceptance of the Bills of Exchange

4. All the trade documents are with the Remitting bank. So now the remitting bank has to prepare a cover letter . Whatever instructions given in this collection order by the exporter which is called the collection instructions will be transferred over to the remitting bank.

5. The Remitting Bank will then forward all the documents to the Collecting/Presenting Bank. Normally there are 2 banks here – the collecting bank is the remitting bank’s agent whereas the presenting bank is the importer’s bank. For simplicity sake in this diagram, both banks are placed into the same box.

So when the documents arrive at the Collecting/Presenting Bank, the Collecting/Presenting bank will then inform the importer and that the instruction is to release the documents against acceptance – which means the importer will have to go to the bank to accept the bill of exchange by signing on the face of the Bill of Exchange

6. Once the importer accepted the Usance Bills of Exchange .The Collecting/Presenting bank will then release the trade documents to the importer. In the meantime, the goods has arrived at the port, and with the trade documents the importer will be able to clear the goods from the port. Once the Importer is able to clear the goods from the port, the Importer will distribute goods out to their retailers and subsequently received payment from their retailers for the goods.

7. On maturity of the Bill of Exchange , which is after 90 days after the acceptance of the Bill of Exchange ,the importer will make payment to the bank

8. The Collecting/Presenting bank subsequently remits payment to the remitting bank.

9. When the remitting bank received the payment, the remitting bank will credit the payment to the exporter’s account.

This entire transaction is governed by the Uniform Rules for Collection URC522 which is published by the International Chamber of Commerce.

So this is in essence the workflow of a Documents Against Acceptance method.